Costco’s Consistency Is Becoming Its Competitive Weapon

In a retail environment shaped by cautious consumers and persistent price sensitivity, Costco continues to stand apart. The company’s first-quarter performance highlights a model that does not rely on promotional spikes or aggressive expansion, but on scale, efficiency, and an unusually loyal customer base.

For investors, the appeal lies in predictability. Membership-driven revenue, disciplined margins, and steady cash generation create resilience even when broader consumer trends soften. Costco’s growth story is not about acceleration, but about durability—an increasingly valuable trait in a late-cycle consumer landscape.

How was the last quarter?

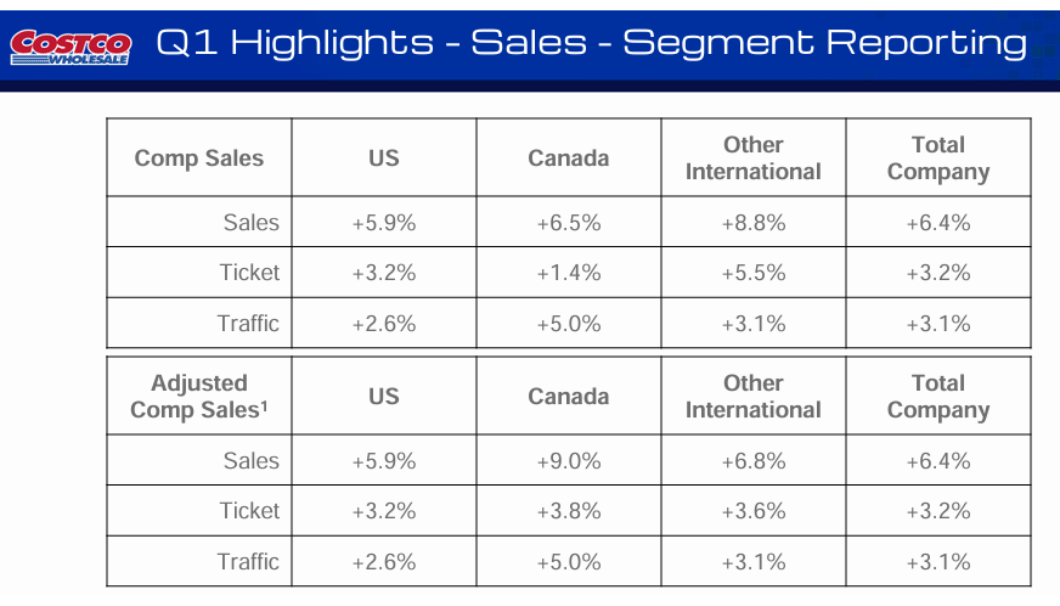

Costco $COST grew total revenue to roughly $67.3 billion in the first fiscal quarter of 2026, with merchandise sales alone up just over 8%. Growth was primarily driven by higher traffic and solid comparable sales growth across regions. Another positive signal was the very strong growth in digitally supported sales, which grew significantly faster than brick-and-mortar stores.

Membership fees reaffirmed their role as a key stabilising element of the business. Membership revenues increased year-on-year and remain highly profitable, allowing Costco to keep merchandise prices low while generating a stable operating profit. It is this model that has been the company's long-term competitive advantage.

Net income in the quarter was approximately $2.0 billion and earnings per share rose to $4.50. Results were partially impacted by a tax benefit related to employee stock-based compensation, but even after adjusting for this, performance remains very solid. Operating profit grew at a pace consistent with sales growth, confirming that Costco is managing costs even as it expands its store network.

Management commentary

CEO Ron Vachris ' comments highlighted steady customer behavior and continued emphasis on member value. According to management, Costco is benefiting from consumers' preference for retailers with clear pricing policies and trusted brands during a period of heightened uncertainty. It was also noted that the company does not see a significant deterioration in customer behavior, even in discretionary categories.

Management also confirmed that it is continuing to open new warehouses in a controlled manner and invest in logistics and digital infrastructure. The goal is not to maximize short-term profit, but to strengthen the long-term relationship with members and improve operational efficiency.

Outlook

Costco does not provide a detailed quarterly outlook, but management comments suggest cautious optimism. The company expects continued solid revenue growth driven by a combination of new stores, steady comparable sales and growth in the membership base. Consumer demand and cost inflation, particularly in wages and transportation, remain key drivers.

From an investor perspective, it will be important to watch whether Costco can maintain its membership growth rate and whether digital sales remain a strong complement to the traditional warehouse model.

Long-term results

Costco's long-term performance shows a clear upward trend. Revenues have increased steadily over the past few years and the company has been able to grow even in periods when the retail industry has faced significant pressures. The rate of growth is not extreme, but it is very consistent, which is key for a company of this size.

Operating profit and pre-tax profit have been rising over the long term, suggesting that Costco can scale its model without significantly impairing efficiency. Net profit has also increased gradually, although the rate of growth fluctuates depending on cost factors and tax effects. Importantly, the company maintains a strong ability to generate cash.

From a debt perspective, Costco remains very conservative. Debt is relatively low relative to the size of the company and is well covered by operating cash flow. Thus, the balance sheet provides ample room for further expansion, warehouse investment, and potentially increasing returns to shareholders.

News

Costco has continued to expand its warehouse network and strengthen its online sales channels in the recent period. At the same time, the company's long-standing Kirkland private label remains one of its primary tools for maintaining member loyalty and differentiation from competitors. International expansion has also played a significant role, particularly in Asia and Europe, where Costco is gradually increasing its presence.

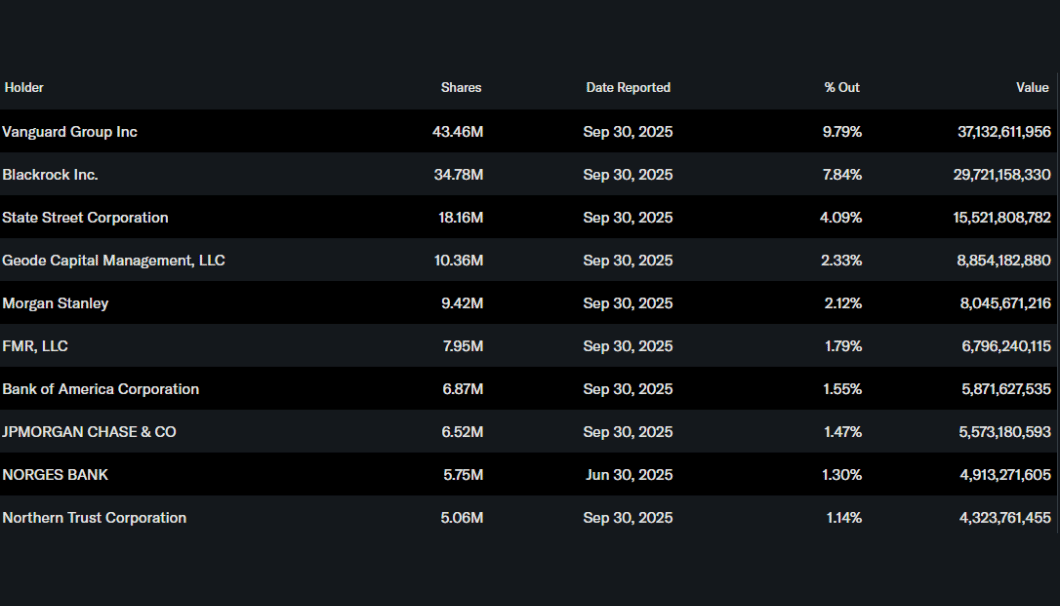

Shareholding structure

Costco's shareholder structure is predominantly institutional. Approximately 72% of the shares are held by institutional investors, dominated by Vanguard Group, BlackRock, State Street and Geode Capital. The proportion of insiders is very low, which is common for an established company with a broad shareholder base. The shareholder structure suggests strong long-term capital confidence.

Analysts' expectations

Analysts view Costco as a quality defensive title with long-term stable growth. The stock's valuation has traditionally been higher than most retail competitors, reflecting confidence in the business model, stable cash flow and strong brand. The company's ability to sustain membership growth and manage cost pressures without disrupting pricing remains a key theme going into the next few quarters.

Zmíněné akcie

Tento článek byl napsán a zkontrolován podle redakčních standardů Bulios.

Sledujte Bulios na Google Zprávách

Buďte mezi prvními, kdo se dozví o nových analýzách, zprávách a pohybech na trzích.